National Savings & Investments (NS&I), as an arm of HM Treasury, has always offered savers a secure home for their money. Unlike deposits made with a bank or building society, which are only protected up to £85,000 under the Financial Services Compensation Scheme (FSCS), deposits with NS&I benefit from unlimited protection, effectively being guaranteed by the UK government.

Although offering unrivalled security, the rate of interest paid on NS&I’s range of accounts has been lacklustre over recent years, being less than 1% per annum for much of the period since 2016. Furthermore, until recently, the selection of accounts offered by NS&I has steadily dwindled, and the eligibility criteria for those that remain have become stricter.

However, following a series of successive rate rises in the Bank of England base rate, some of the existing NS&I accounts have become more appealing propositions, and previously discontinued accounts have been reintroduced.

For individuals with large cash sums, and for whom long-term investments might not be appropriate, NS&I now represents a viable option. This is particularly the case for personal injury investors (including deputies and trustees) who have received a significant amount of compensation and need to set aside capital temporarily, whether to meet near-term expenditure or with a view to phasing money into an investment portfolio over a period of time.

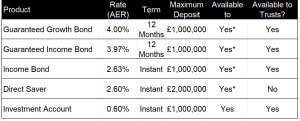

The following table summarises the NS&I accounts currently on-sale that have a high maximum deposit limit, indicating which of these are available to deputies and trustees:

* If beneficiary is 16 or over

Whilst there are limits on the amount that can be deposited into each account, it is possible to hold one of each type of account (assuming that the eligibility criteria for each account are met), meaning that in many circumstances it is possible to deposit a sum of up to £6,000,000 in the knowledge that the money is absolutely safe, whilst still earning a reasonable return.

It is important to note that savers are subject to the risk that the returns will not keep pace with inflation, particularly in the present climate. However, where generating a real return is secondary to the primary objective of capital preservation, NS&I is a worthwhile consideration.

We will be happy to have a no obligation discussion, or e-mail us at: picop@chasedevere.co.uk or visit our website at www.chasedeverepicop.co.uk